I’m a big proponent of having a bank president or CEO craft his or her own message, especially if it’s for the troops or customers. According to our research with email newsletters, the President’s Message or CEO’s Letter always scores extremely high. In fact, it wipes out all the other articles in the newsletters as far as readership numbers. That’s why I always encourage bank execs to author their own communiqués. The message rings with authenticity and readers get to know the person behind the suit.

But there is one time when I suggest you rethink this strategy. . . that’s when an established publication comes calling and asks for an article as an expert in your field. First, a good article takes time. There’s research, plus the writing and editing. You could literally invest hours and hours in the project. You may not have the luxury of penning your thoughts. Second, if you’re not an accomplished writer, you could be in for a rough patch. Most important, you’ll want to maintain your reputation. I’ve seen a number of CEO essays where readers wondered about the author’s credentials due to poor sentence structure, confused logic and uninteresting content. So how can you maintain your expert standing yet polish your prose? Hire a ghostwriter!

What can a good ghostwriter do for you? The writer can. . .

Save you time. Your time’s at a premium. A writer can carry the heavy writing load and bring you a draft for approval and revisions.

Gather the important ideas and facts, plus do additional research if needed. Then organize those fragments into a logical, coherent article. A really great writer can run with any nugget of info and polish it into a real gem.

Replicate your style into the writing so it sounds original and incorporates your personality. After all, you’d like to instill some of your personality into the piece if it calls for it.

What you should look for in a ghostwriter?Sharp, quality writing that engages the appropriate audience. Your ghostwriter’s samples will give you a clue. Is the writing intriguing? Does it hold your interest? Is it easily understood?

Experience & knowledge. Look for someone whose background you feel comfortable with. Depending on the type of article, you’ll want someone who has knowledge or experience in your field. Look for someone who can relate to the audience or express a complex subject with simplicity. If the person is more knowledgeable about your topic, the less time you’ll need educating them. That writer will just be able to run with your topic. Remember, the more knowledgeable the person, justifiably the higher the fee.

Compatibility. You’ll accomplish more if the two of you are on the same wavelength. Establish a good relationship at the beginning of the process and you’ll be working from an advantage.

Getting the best possible written results. If you follow a few simple caveats, the process will be smoother and the results will be sharper. You’ll have a running start if you. . . Identify your goals for the article. Do you wish to educate, state an opinion, inspire or encourage?

Explain the task. Do you have a topic in mind? All the better. Do you have any background material to share about the topic, resources to recommend or information about the publication? What’s the deadline, word count or other specifics the publication has mandated? The more you have ready, the faster and more smoothly the project will progress. You may even wish to outline the topic or prepare a rough draft. Don’t have a specific topic? At the very least, offer the writer some direction, otherwise you both will just be frustrated and spinning your wheels. On the other hand, find an extremely knowledgeable writer in your field and that person may be able to suggest appropriate topics.

Be willing to let the writer do his or her job. If you do write that first draft, be willing to accept changes. That’s why you hired a writer. A professional is able to view the topic from the reader’s viewpoint. You may be too close to the situation to see it from various angles. Too many times I’ve seen execs change the copy back to their original version. A good writer doesn’t mind being corrected, especially if there is an error. But you’re defeating the purpose of using a professional writer if you go heavy on the edits.

Define the audience for the writer. Are you writing for the Harvard Business Review or a Junior Achievement magazine? You’ll want someone who can match the content of those publications.

Outline the specifics you want to include in your article. . . any quotes, stats, keywords.

Spend some time with the writer. If it’s important that your personality come through in the article (esp. in a journal where people know you), spend some time with the writer so he can judge your style of expression. An experienced writer can pick up on your personality and express it in the article. You don’t want an inexperienced writer literally putting inappropriate words in your mouth or writing from their perspective. I once read an article “authored” by a male bank president in which the writer used expressions that would have definitely been used by a female writer.

Don’t pass the finished article through a committee or group for their feedback. Fine, if you need to go through compliance. But send it through the meat grinder and you’ll come up with incoherent hash. You hired a pro, trust that person.

You don’t need to be a bank president or CEO

to hire a ghostwriter.Even bank marketing execs, lenders, branch managers, or commercial bankers may be asked to pen a few words for a publication. If it means maintaining the bank’s reputation, don’t fear hiring a ghost writer.

Related articles in Bank Marketing:

What can the “President’s Message” do for your marketing?

While other banks were issuing letters and written statements about the state of their financial institutions, Bill Carr, president and CEO of

While other banks were issuing letters and written statements about the state of their financial institutions, Bill Carr, president and CEO of

arious marketing materials for my clients, I’m instructed by their compliance departments to include diverse clientele and employees. In other words, a microcosm of our society. No problem with that. Mumbai-based YES Bank (which I introduced in my

arious marketing materials for my clients, I’m instructed by their compliance departments to include diverse clientele and employees. In other words, a microcosm of our society. No problem with that. Mumbai-based YES Bank (which I introduced in my

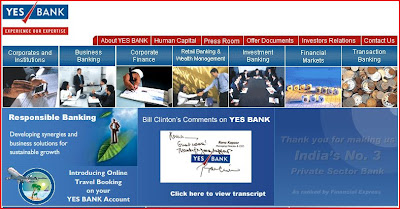

I’d call it a pretty good marketing coup when a bank has an actual endorsement by a former President of the United States on its website’s homepage. And, that what this Indian bank, aptly named

I’d call it a pretty good marketing coup when a bank has an actual endorsement by a former President of the United States on its website’s homepage. And, that what this Indian bank, aptly named  The homepage allows for a pop-up so the website visitor can read the actual transcript of President’s Clinton’s message to the bank’s founder. In fact, Clinton used the YES BANK’s calling card to pen his personal hand-written message. . . even better. The note is in response to the bank’s backing of the

The homepage allows for a pop-up so the website visitor can read the actual transcript of President’s Clinton’s message to the bank’s founder. In fact, Clinton used the YES BANK’s calling card to pen his personal hand-written message. . . even better. The note is in response to the bank’s backing of the

In the release, Terry Zink, executive vice president and head of Retail and Affiliate Administration, noted that

In the release, Terry Zink, executive vice president and head of Retail and Affiliate Administration, noted that  Having developed and written kids’ savings newsletters, I do like the 10 points listed in the bank’s

Having developed and written kids’ savings newsletters, I do like the 10 points listed in the bank’s